Sector Spotlight: Women's Health

Disclaimer: The below aims to share an overview of my findings so far on the women’s health landscape from the perspective of a Canadian minority growth investor. If you are a founder in the space or a subject matter expert, please reach out - I’d love to connect!

What is Women’s Health?

Women's health is a multifaceted field that encompasses a broad range of products and services designed to address the unique health needs of women throughout their lives and as they cross into different life stages. This sector, sometimes referred to as "FemTech," includes health issues experienced solely, differently, or disproportionately by women. The term is primarily used to denote tech-enabled, consumer-centric solutions addressing women's health, and usually excludes pharmaceuticals.

Why Should We Talk About Women’s Health?

While healthcare is commonly associated with diagnostics and treatments for specific health concerns, women experience distinct stages throughout their lives that require various unique interactions with the healthcare system. This evolving need has led to growing recognition of Women’s Health as its own category.

In conjunction with women’s unique health needs, women consume 80% of pharmaceuticals1, incur 80% higher health expenses compared to men in the same age group2, and utilize preventative care services at a higher rate than men (in the US)3. And this is also despite being consistently under-represented in clinical research4.

Several societal trends also support an increased focus on women’s health in recent years. These include:

Technological Innovation – growing technological advancements and innovations across research, medical devices, and patient engagement tools allowing for greater access to care and improved outcomes

Lifestyle Changes – global tendency towards later pregnancies resulting in greater demand for fertility treatments and related services to support reproduction

Declining Sperm Counts – human sperm counts have decreased by over 50% in the past 50 years resulting in greater fertility challenges

Aging Population – 6,000 women in the US reach menopause every day5 increasing the need for menopausal and post-menopausal treatments and support

Cultural Shift – growing trend towards wellness, increased health-consciousness, and awareness of various services and offerings available

And investors have taken notice - funding for women's health startups has seen a significant increase in recent years, from approximately $500 million in 2020 to over $1.1 billion in 2022. This growth has also remained resilient amidst a broader pullback in digital health funding.

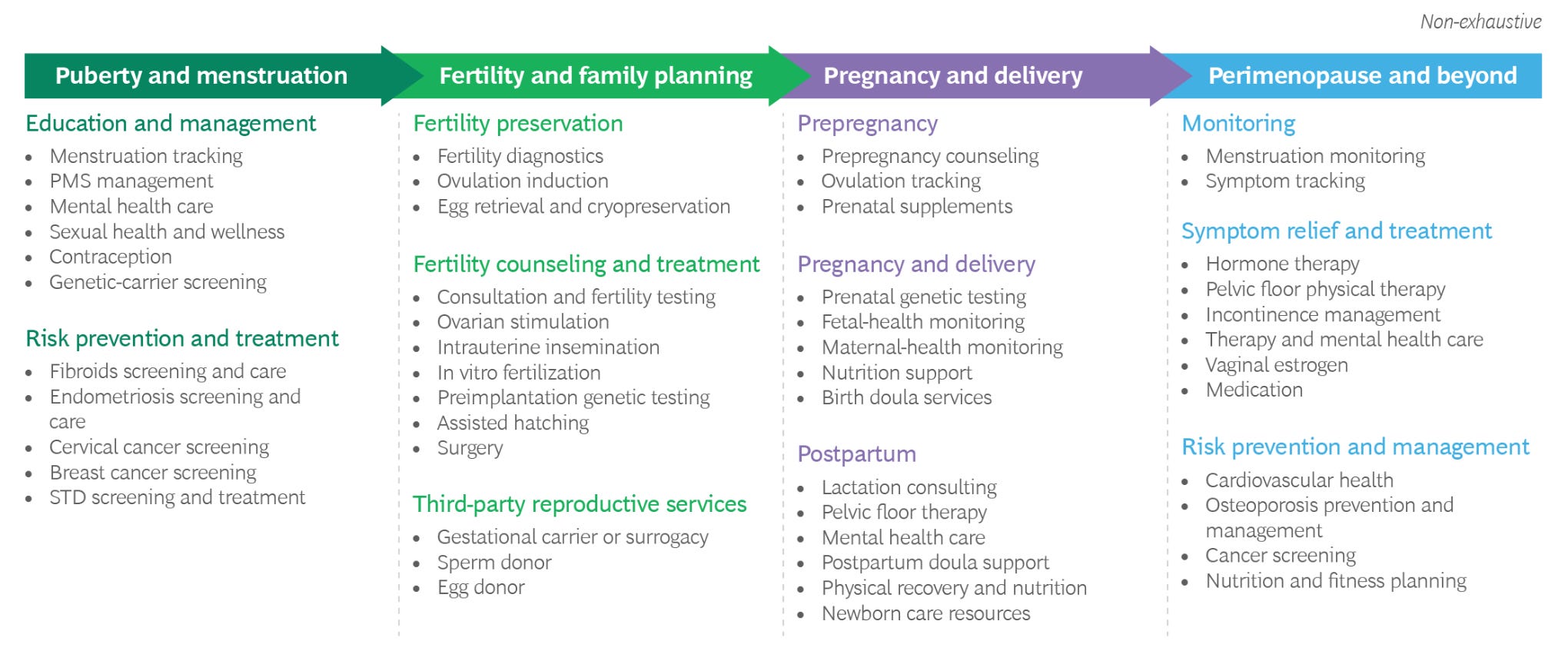

What Are The Main Segments Encompassed Within Women’s Health?

The women's health category can be divided into several key segments:

Reproductive Health and Fertility: This segment focuses on solutions for family planning, contraception, fertility tracking, assisted reproductive technologies (ART), and innovative approaches to enhancing fertility treatments

Maternal Health: This segment includes products and services catering to the needs of pregnant women, such as prenatal care, remote monitoring, maternal health diagnostics, childbirth preparation, and postpartum support

Menopause: This segment aims to improve the quality of life for women experiencing menopause by offering hormone therapies, lifestyle interventions, and specialized health products to manage symptoms and reduce associated health risks

General Women's Health: This segment addresses concerns and diseases that affect women specifically or disproportionately

Mental Health and Wellness: This segment includes digital platforms and therapies addressing mental health challenges specific to or frequently affecting women, such as perinatal and postpartum depression, anxiety, and eating disorders

What Does The Women’s Health Landscape Look Like For A Growth Investor?

While a variety of intriguing business models exists across the entire Women’s Health category, the Reproductive Health and Fertility segment stands out as a particularly interesting area for investment among growth and private equity investors. This is attributed to a combination of attractive market tailwinds and business model economics.

As with many aspects of healthcare, business model innovations progress slowly. Within Reproductive Health and Fertility, traditional fertility clinic roll-ups and egg and embryo freezing services have continued to dominate private equity investments. However, Mate Fertility, a venture-backed startup, is attempting to pioneer a new approach that involves upskilling OBGYNs into IVF practitioners and establishing a pathway for physician-owned clinics within a broader franchise model. This model aims to optimize for scalability in a space suffering from growing wait times amidst increasing demand.

At the earlier and more ambitious stages, several startups are finding solutions to make the IVF process more affordable and accessible by addressing one of the toughest parts of the process—successful implantations. Notable Canadian companies like Future Fertility and Juniper Genomics are working to close this gap in fertility treatment.

While the Women’s Health category has received significant VC investment in recent years in the US, (Maven Clinic being an example of a behemoth in the space) leading to a wide landscape of later-stage investment opportunities, the Canadian landscape is still very much in its nascent stages.

What Are Some Challenges Facing Women’s Health Startups?

Fertility Dominance: The Fertility segment, and IVF-related businesses specifically, often overshadow the other segments within Women’s Health

Investors looking to invest in the Women’s Health category should expand their scope to include looking at the other segments as the IVF space becomes more saturated

Neglecting Financials in Pitches: Founders, particularly those in the early stages, sometimes neglect communicating the economic viability of their ventures in their pitches. This dynamic can also feed into the stigmatization of investments in Women’s Health as philanthropy vs the very real economic returns that could be generated

While revolutionary ideas are essential, founders should keep in mind that investors, driven by the need to generate returns, require a clear understanding of how your startup plans to commercialize and generate revenue

Point-Solution vs Platform: Women’s Health startups today are primarily point solutions (e.g., postnatal support tool, doula services marketplace) with very few platform solutions or those that can seamlessly connect to primary care providers

Point solutions often have smaller TAMs and a weaker ability to scale. As the category matures, I believe we can expect to see consolidation in the space as investors bet on a winning horse to build a platform around. I also believe that a successful platform will require the ability to seamlessly offer both in-person clinical services as well as digital services

Regulatory Hurdles for Medical Device Startups: Medical device-based startups often face significant challenges with respect to regulatory approvals which can delay commercialization and result in a very long time horizon between investment and revenue

A VC-style investor may not always be the right type of investor for these kinds of business models due to the way the venture model works. Founders may find more success in angel, strategic, or government-back funding. For further reading on this topic, I recommend Christina Farr’s fantastic article titled “Resetting expectations for VC investing in health tech”)

At Maverix, we are eager to engage closely with the Women's Health ecosystem and find ways to support Canadian founders through our expertise, network, or investment, should there be an opportunity that aligns with our mandate.

If you are a founder in the space, please reach out! We would love to meet you and continue to build on our Women’s Health knowledge.